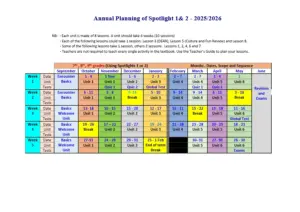

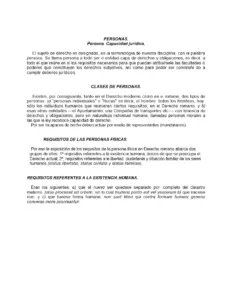

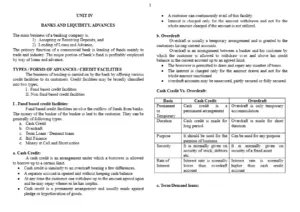

Accounting for Special Transactions by CA Sanket Shah provides a comprehensive overview of various financial instruments and their implications in business law. It covers essential topics such as bills of exchange, promissory notes, and demand bills, offering insights into their definitions and applications. The document is designed for accounting students and professionals seeking to understand the nuances of special transactions in accounting. Key concepts include the renewal of bills, noting charges, and the retirement of bills, making it a valuable resource for exam preparation and practical application in the field of accounting.

Key Points

- Explains the fundamentals of bills of exchange and promissory notes in accounting.

- Covers the process of renewing bills and the implications of dishonored bills.

- Details the accounting entries for genuine and accommodation bills.

- Discusses the sale of goods on approval or return basis and its accounting treatment.