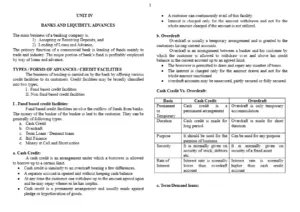

The Division of the Ledger provides a comprehensive overview of financial ledgers, including the Sales Ledger, Purchases Ledger, and Nominal Ledger. It explains how these ledgers track money owed to and by businesses, detailing the processes involved in managing credit sales and purchases. This resource is essential for accounting students and professionals looking to enhance their understanding of financial record-keeping. Key features include examples of customer and supplier accounts, control accounts, and the flow of transactions. Ideal for those preparing for accounting exams or seeking practical insights into ledger management.

Key Points

- Explains the structure and purpose of the Sales Ledger for tracking customer debts.

- Details the Purchases Ledger for managing supplier accounts and payments.

- Describes the Nominal Ledger as the main accounting record for non-personal accounts.

- Includes examples of ledger entries and control accounts for accuracy in financial reporting.