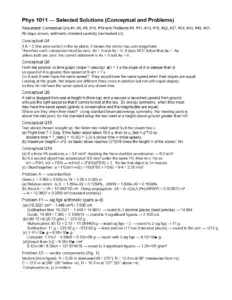

Solution to Model Question 2077 3

ii. Outstanding rent Rs 5,000

Required: Adjusted trial balance

Ans: ATB Total Rs 7,55,000

SOLUTION

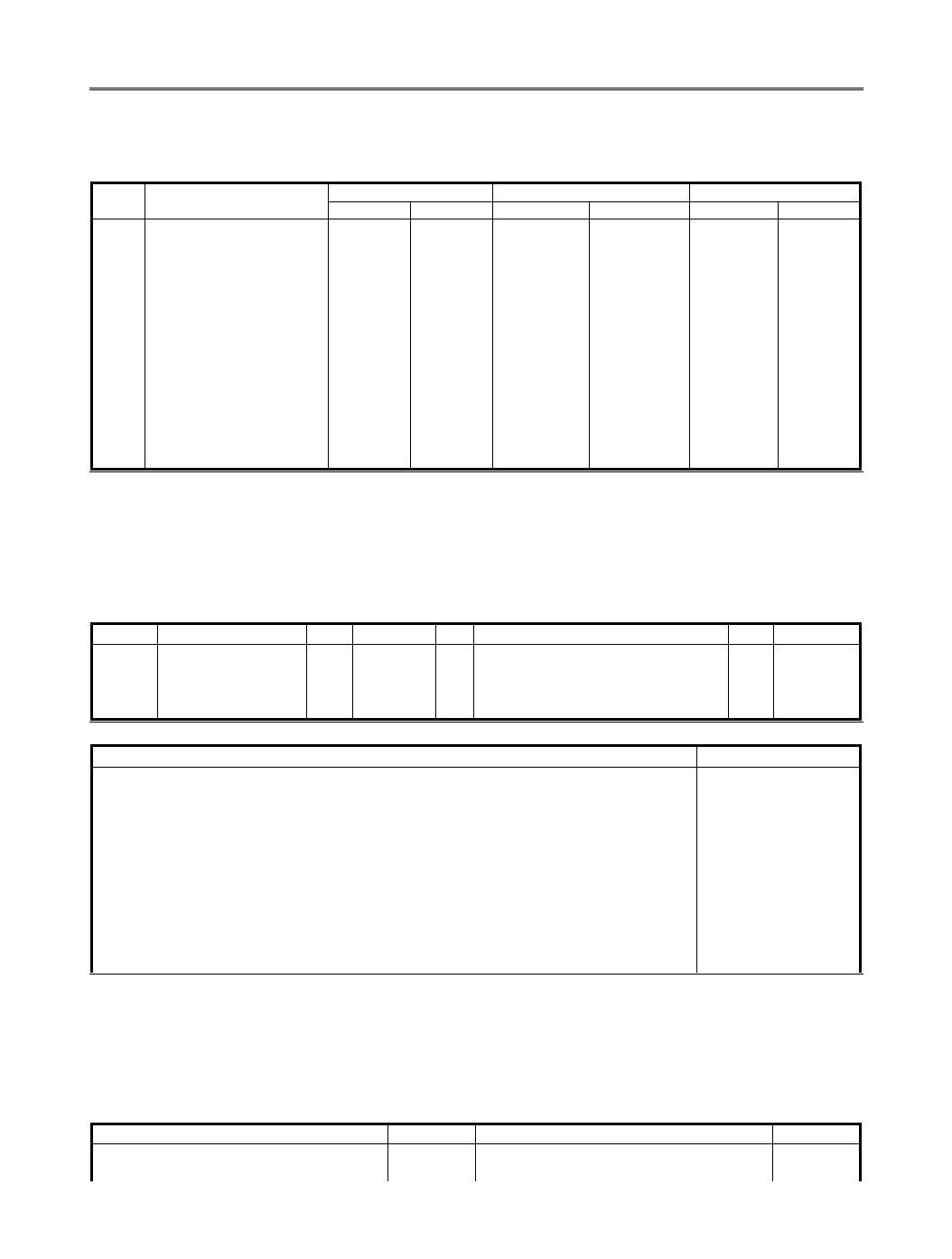

Adjusted trial balance

S.N Particulars Unadjusted Adjustment Adjusted

Dr. Cr. Dr. Cr. Dr. Cr.

1 Capital - 200,000 - - - 200,000

2. Creditors - 50,000 - - - 50,000

3. Sales - 450,000 - - - 450,000

4. Bank overdraft - 50,000 - - - 50,000

5. Furniture 150,000 - - 15,000 135,000 -

6. Cash at bank 160,000 - - - 160,000 -

7. Debtorss 40,000 - - - 40,000 -

8. Rent 25,000 - 5,000 - 30,000 -

9. Wages 5,000 - - - 5,000 -

10. Purchases 350,000 - - - 350,000

11. Salary 20,000 - - - 20,000

Adjustment

i. Dep

n

on furniture - - 15,000 - 15,000 -

ii. Oustanding rent - - - 5,000 - 5,000

Total 750,000 750,000 20,000 20,000 755,000 755,000

b. Following information is provided:

i. During the year the bad debts amounted to Rs 5,000

ii. Debtors at the end of the year were Rs 200,000 and maintained 5% provision.

iii. Opening provision for doubtful debt Rs 6,000

Required: Provision for doubtful debts account.

Ans: Estimated bad debts Rs 9,000

SOLUTION

Dr. Prov. for doubtful debt A/C Cr.

D Particulars LF A D Particulars LF A

To debtors 5,000 By balance b/d 6,000

To balance c/d 10,000 By estimated bad debt exp. 9,000

[5% of 200,000]

15,000 15,000

16. Following incomes and expensese were taken from a company as on 31st Chaitra last year given below:

Particulars Cr (Rs.)

Rent expenses 36,000

Sales revenue 4,50,000

Purchase 1,60,000

Wage 8,000

Salaries expenses 26,000

Selling expenses 9,000

Opening stock 20,000

Interest expenses 5,000

Other expenses 7,000

Prepaid insurance 8,000

Additional information:

i. Closing stock Rs 45,000

ii. Prepaid insurance was expired Rs 3,000

Required: Trading and profit and loss account

Ans: GP Rs 3,07,000; NP Rs 2,21,000

SOLUTION

Trading & PlL A/C

For the year ended 31

st

Chaitra, last year

Particulars Amount Particulars Amount

To opening stock 20,000 By sales 450,000

To purchase 160,000 by closing stock 45,000