Amalgamation Concepts for SEM VI explores the principles of amalgamation, absorption, and external reconstruction in corporate finance. This document provides detailed explanations of the processes involved in merging companies, including the formation of new entities and the dissolution of existing ones. It is designed for students studying corporate finance and accounting, particularly those preparing for examinations in 2025-26. Key topics include the accounting treatment for amalgamations, journal entries, and statutory reserves.

Key Points

- Explains the process of amalgamation and its implications for existing companies.

- Covers absorption and external reconstruction with practical examples.

- Details the necessary journal entries for accounting during amalgamation.

- Discusses statutory reserves and their importance in the amalgamation process.

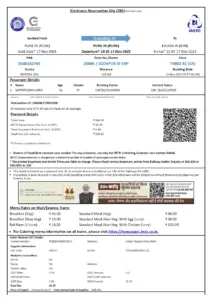

Purchase of Business")