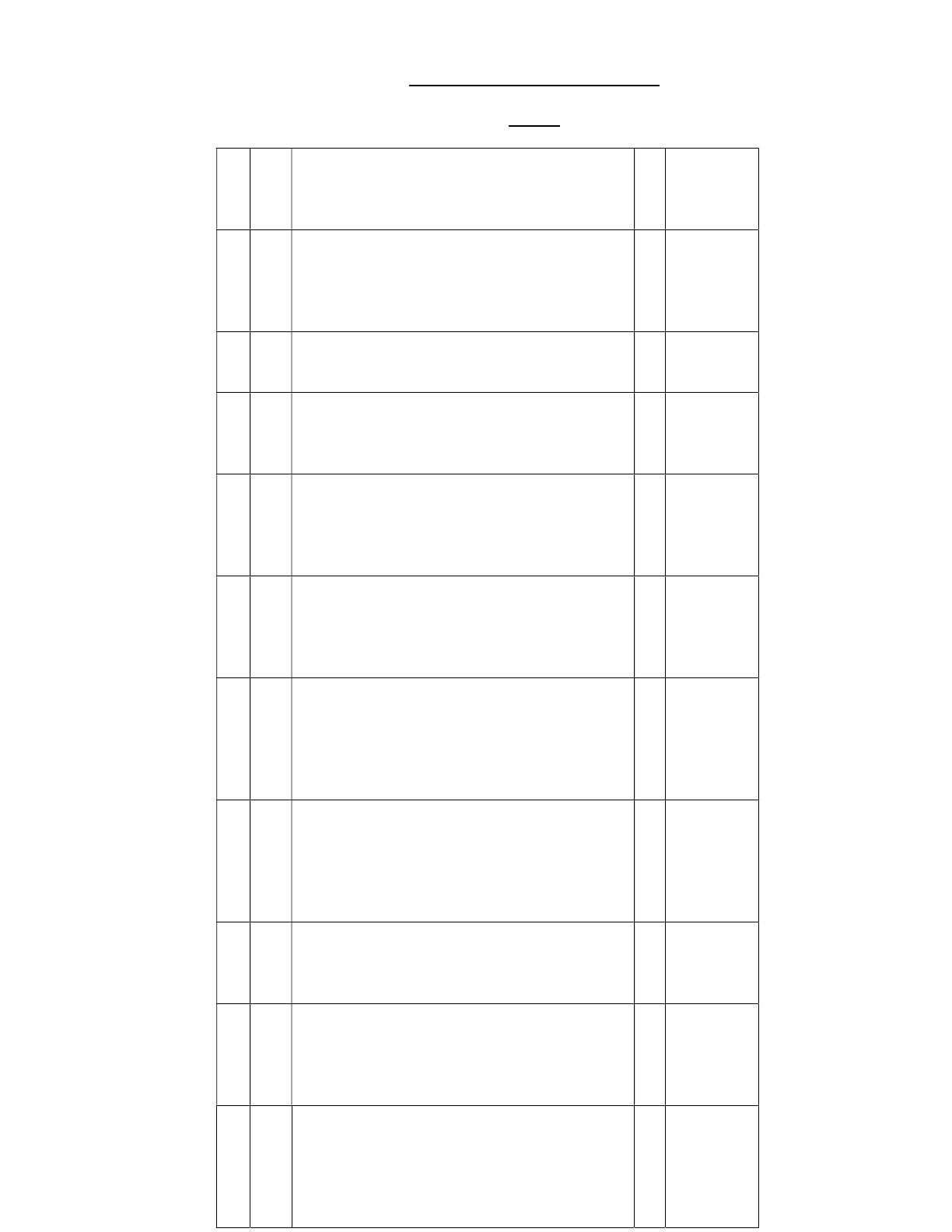

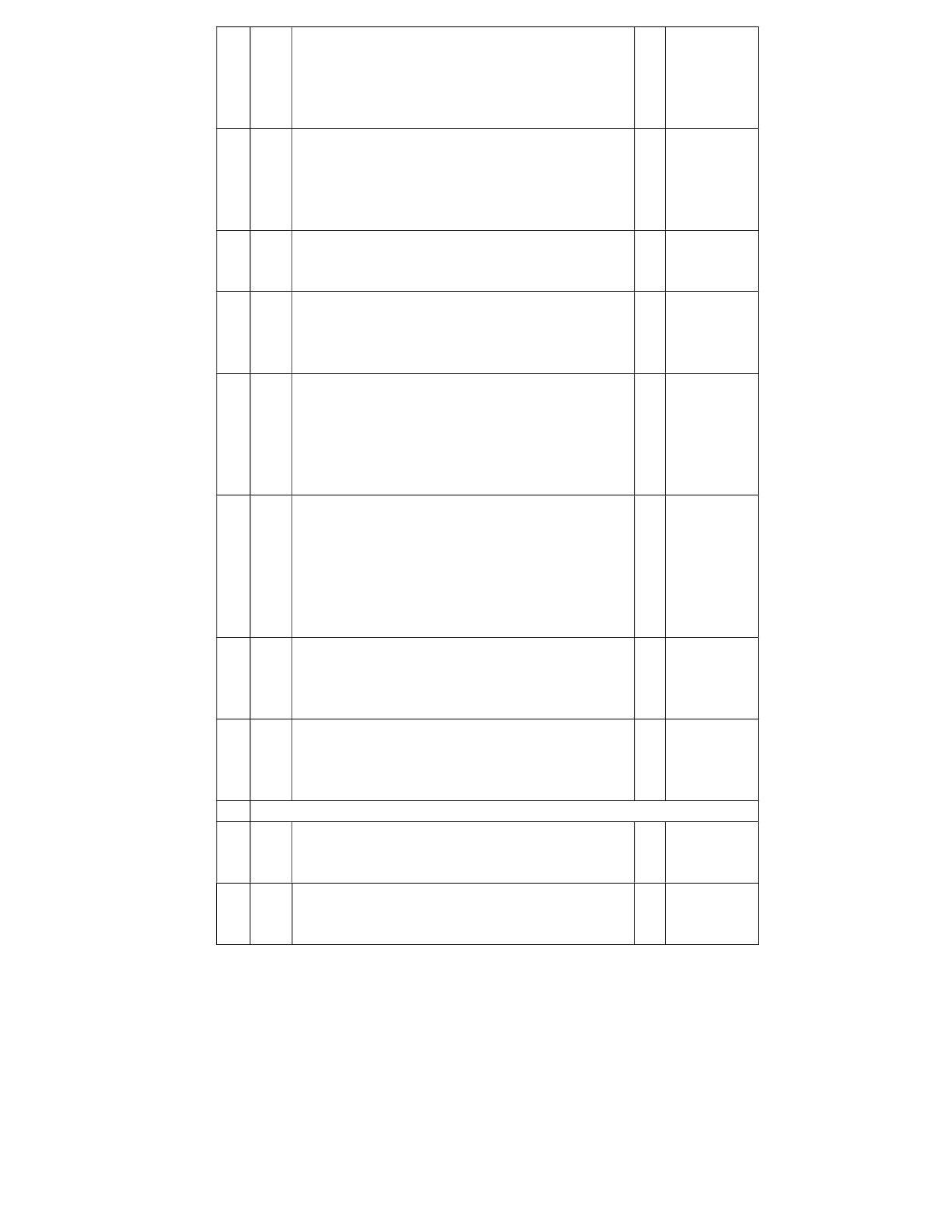

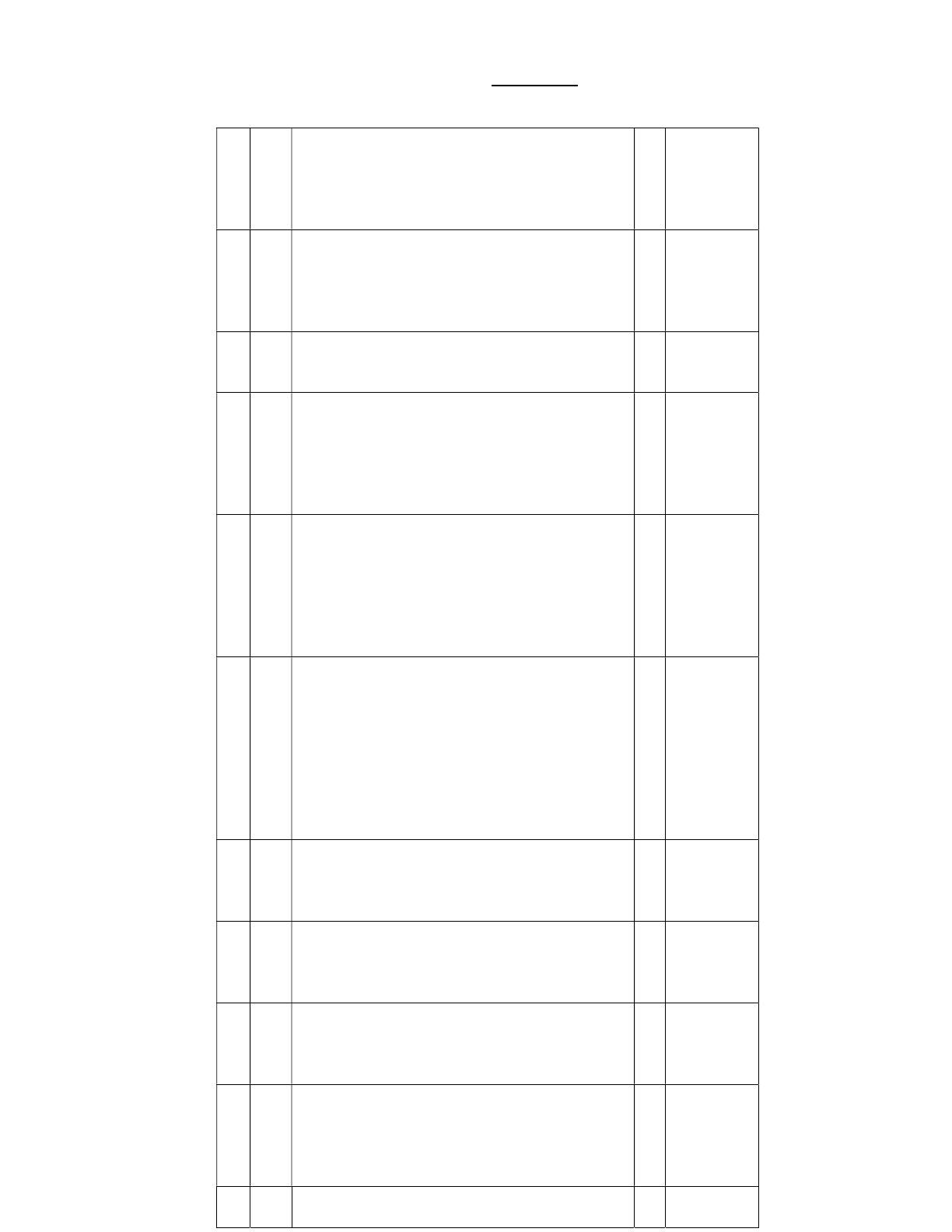

Journal entries for accounting transactions provide a comprehensive overview of how to record various financial activities. This document includes detailed examples of share applications, allotments, and debenture transactions, making it essential for accounting students and professionals. It covers key concepts such as share capital, call money, and interest calculations, offering practical insights for real-world applications. Ideal for those studying accounting principles or preparing for exams, this resource serves as a valuable reference for understanding journal entries in financial accounting.

Key Points

- Explains the process of recording share applications and allotments in accounting journals.

- Covers debenture transactions, including application money and interest calculations.

- Details the treatment of forfeited shares and their impact on capital reserves.

- Includes examples of journal entries for various accounting scenarios, enhancing practical understanding.